Why ignorance is not bliss for financials

Financial stocks made up 26%^ of the global share market index before the Global Financial Crisis.

That’s now down to around 15%* today thanks to a shake in the sector and ‘de-yielding’ of the global monetary system.

The sector heavyweights of the banking fraternity have experienced a general de-rating with many investors turning away from the sector.

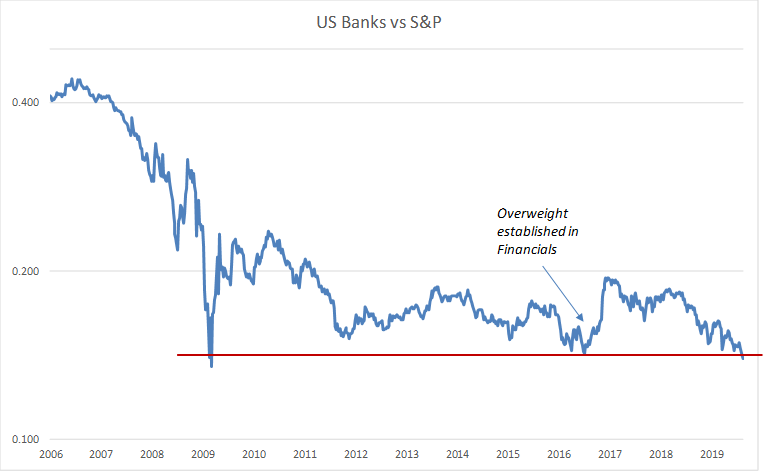

US banks — which form a large part of the global banking segment — have materially underperformed the market since the GFC.

They are now back to levels last seen in 2009 and 2016 as you can see in the following chart which tracks the relative performance of US banks against the broader US equity market.

US Banks now at pre-GFC levels

Source: Bloomberg, Pendal using representative exchange traded products

In mid-2016 at the inception on the Pendal Concentrated Global Share Fund we formed a view on a range of major influencing factors including Brexit, interest rates and inflation.

This led us to take a deeper review of the sector to identify areas of interest.

We already knew that many of the sector’s participants were well established with considerable economic moats and scale. This research culminated in establishing material positions across the financials sector.

Within the banks we favoured the regional players over the globally focused competitors which typically have significant investment banking exposures.

This led to positions being established in Wells Fargo, Lloyds Banking Group, Caixa Bank and KBC Group.

The banks we hold are of higher quality as they have generated higher returns than their peers through scale-driven cost efficiencies.

This has enabled them to build the capital required by regulators and be in a position to return the remaining free cash flow in the form of dividends and buybacks to shareholders during a tough environment.

Considering the regional nature of these businesses we expect this cohort will continue to exhibit a degree of resilience should the broader banking sector experience further de-rating.

However, if the broader environment does instead improve, we expect these companies to outperform the market much like they did following the dislocations in 2009 and 2016.

Stock exchanges – the forgotten financials

The other often overlooked segment of Financials are stock exchanges.

Stock exchanges generate revenue based on trading volumes, with an inter-related link to market volatility.

As market uncertainty develops, the derivative products issued by exchanges tend to generate higher revenues as a function of increasing spreads on pricing as well as through higher trade volumes.

Market volatility remains depressed and near historically low levels.

This negatively impacts revenue for companies like CME Group — operator of the Chicago Board of Exchange which holds a 90% market share in global futures trading and clearing services.

We launched the Fund with half of the financials exposure held in stock exchange operators.

This has made a strong contribution to the Fund’s returns over the period. Collectively, our investments in stock exchange operators have generated an average annual return of 23% (in Australian dollar terms).

In December 2018 we took profits on one of these businesses — Intercontinental Exchange — after the stock reached our valuation threshold of a 5% buyout yield.

Staying true to form

Stock exchanges remain a centrepiece of the Fund’s financials exposure and we expect these stocks to continue to re-rate as market volatility increases.

Our process is designed to identify fundamentally sound companies which have been flat or underperformed for a number of years.

Of course, the present environment is far from certain for banks in the short term amid the macro policy tensions but, from a long term perspective their valuations remain compelling to us.

At these levels history has shown it can be beneficial to look through the immediate market concerns and noise and invest in high quality companies wherein their intrinsic value is not being reflected in their current stock price.

^ Source: Bloomberg. Financials weight as represented within the MSCI World Index as at 31 December 2016.

* Source: Bloomberg. Financials weight as represented within the MSCI World Index as at 31 August 2019.