Why Crispin Murray expects equity markets to keep rising

Our head of equities Crispin Murray makes the case for a continued rise in equity markets in a presentation to Portfolio Construction Forum’s Markets Summit. Here’s a quick summary.

Key points

- Government stimulus and accommodative monetary policy driving stock markets

- Policy push to lift wages and reduce inequality

- Focus on clean energy and economic resilience

A DESIRE to correct the policy mistakes of the post-GFC era should underpin a continued rise in equity markets as the global economy recovers from COVID-19, believes one of Australia’s most experienced portfolio managers.

A unique combination of supportive government policy and the re-opening of the global economy should unleash of a wave of pent-up demand for consumption and investment, driving stock markets to new highs, believes Crispin Murray, who heads up one of Australia’s biggest equities teams at Pendal.

Unlike previous booms, this time governments will tolerate excesses in some parts of the market in the hope of improving wages, reducing inequality and building the infrastructure to support a clean energy future, he believes.

“There’s been a fundamental shift in the motivations and mission of policymakers,” says Murray in a presentation to the Portfolio Construction Forum Markets Summit 2021.

“They have observed what’s happened with the rise of populism, they’ve seen what happened as a result of COVID and they’ve looked back at what happened in the post-GFC era and there are a number of wrongs – a number of policy mistakes – that they are now addressing.

“And in doing that, they’re actually helping to support the equity market.”

Murray identifies three key policy mistakes that governments are seeking to correct:

- The first is inequality, which intensified post-GFC as policymakers kept tight hold of fiscal and monetary policy, while globalisation and the growth of the technology industry kept a lid on real wages.

- The second is a growing fragility in the world economy produced by global supply chains, just-in-time production and finely tuned corporate balance sheets.

- And the third is policy complacency about the environment and the need to move to clean energy, with little urgency to meet carbon emissions targets.

“COVID showed that existential threats can happen and they can happen very quickly.

“These things focus policymakers’ minds. They had to respond to a cyclical issue, but it also focused their minds on these structural issues.”

Policy changes underway

Murray says policy changes are occurring in three areas.

A new era of monetary policy has abandoned containing inflation as a short-term goal in favour of driving social cohesion and full employment.

Real interest rates have been negative for some time and will stay lower over the course of this cycle, says Murray.

Monetary stimulus is also causing money supply growth that has not been seen since after the war.

“When you’ve got that level of stimulus coming into the economy, it has to go somewhere. This is why you’ll see equities benefiting from that sort of monetary policy environment.”

Fiscal policy is also supportive.

“I’d have to go back to World War Two to see anything like this level of fiscal deficit, this fiscal stimulus.

Uniquely, fiscal and monetary stimulus is occurring simultaneously as a decade of fiscal austerity comes to an end.

“It will be supportive for the economy, and for earnings.”

Until now, expansionary policy has been held back by the headwind of the COVID-19 pandemic and its associated government shutdowns.

“But now what we’re seeing is those headwinds turning to tail winds. We’re going to see the excess savings, the benefit of pent-up demand as vaccines are rolled out, you’re going to see continued loose monetary policy and fiscal policy.”

Murray says the stimulus has produced close to US$3 trillion of excess savings in the US alone, equivalent to more than 16 per cent of actual consumption which is the major driver of the US economy.

Meanwhile, available capital in private equity funds and special purpose acquisition companies is at record levels.

As this excess cash starts to find its way into the economy it will drive both higher consumer spending and higher investment.

“There’s going to be an underlying support for the market because of that level of liquidity.”

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

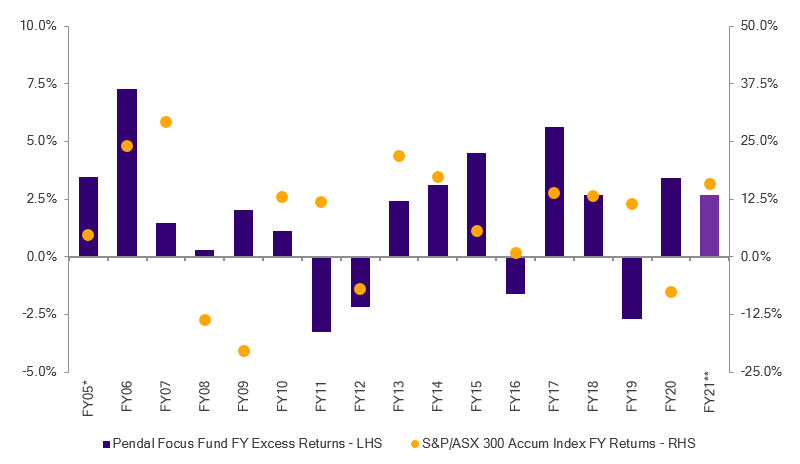

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21.

Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

This article has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and the information contained within is current as at March 05, 2021. It is not to be published, or otherwise made available to any person other than the party to whom it is provided.

This article is for general information purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information in this article may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information in this article is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance.

Any projections contained in this article are predictive and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.