Tim Hext: what to expect now the RBA and Canberra are in lock-step

Here’s our weekly Bond, Income and Defensive Strategies wrap from Pendal portfolio manager Tim Hext (pictured).

Find out more about Pendal’s fixed interest strategies

THERE were plenty of positive signs this week.

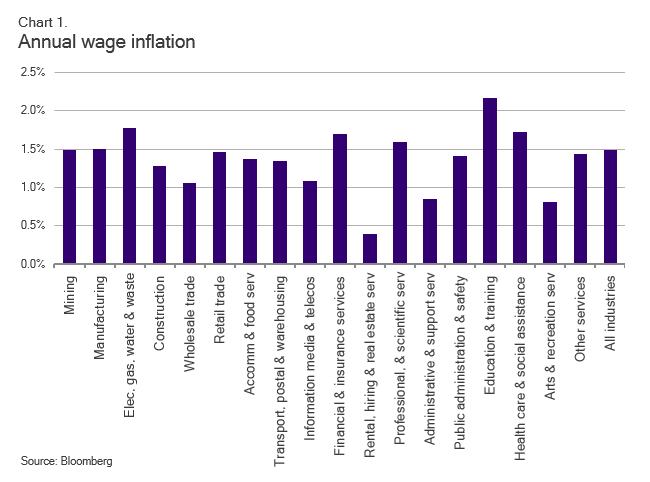

Despite a slight pull-back in the latest job numbers and consumer confidence, we’re seeing wage inflation recover from a down-trend that was underway before the pandemic shock.

April was expected to be more subdued than earlier months because the data now reflects the full impact of JobKeeper ending.

There were plenty of worries that hard won post-Covid gains would be lost as talks of tapering accelerate overseas.

But now there is a difference.

Before the pandemic the RBA acted as a lone wolf, tackling unemployment with monetary expansion, while the federal government kept a lid on spending due to its budget surplus obsession.

Now the RBA and federal government are in lock step as Team Australia.

Fiscal policy is the main game

The pandemic crisis finally freed the Liberal government from the shackles of dogma — Budget surplus at all costs.

The transformation is now complete with the release of the federal Budget.

Employment is now above its pre-COVID level and GDP is expected to soar this year. But the government continues to plough more into the economy, presumably to secure a full employment victory this time.

New stimulus initiatives are worth 4.1% GDP over four years. This compares to the paltry 2019 budget spend worth 0.5% of GDP when unemployment was drifting north of 5%.

These are good signs indeed — not just for the Australian economy but also for the Liberal government.

As the saying goes, fortune favours the brave.

They may learn that not all spending is bad. The good news this time is that the strategy is affordable.

A continued surge in commodity prices — as well as tax receipts from growth instead of higher taxes — will make this a “self-funded” expenditure.

Monetary policy

We anticipate the RBA’s monetary response will remain expansionary to support the federal government’s fiscal response.

That will involve keeping the cash rate target and the interest rate of RBA Exchange Settlement account balances low. It’s also highly likely there will an extension of the Quantitative Easing (QE) program as part of the toolkit.

The incredible rebound in the Australian economy has given the RBA a shot in the arm.

These complementary actions between the monetary and fiscal policies make full employment a goal rather than a dream.

The implications

Despite the stimulatory Budget surplus, a massive increase in supply of Australian government bonds (CGLs) is not anticipated, because the spend can be largely funded through economic growth.

An extension of the RBA’s QE program will continue to provide support.

We therefore continue to favour CGLs versus semi-government bonds as the economy recovers.

We’re also keeping a watchful eye on inflation to see if it will turn structural this time or remain transitory — as was the case in historical post-crisis periods.

As highly expansionary fiscal and monetary policies remain in place after the economy hits full capacity next year, we suspect inflation will stick above target for another few years at least.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here

This article has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and the information contained within is current as at May 21, 2021. It is not to be published, or otherwise made available to any person other than the party to whom it is provided. PFSL is the responsible entity and issuer of units in the Pendal Focus Australian Share Fund (Fund) ARSN: 113 232 812. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling Customer Relations on 1300 346 821 (8am to 6pm Sydney time) or at our website www.pendalgroup.com. You should obtain and consider the PDS before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This article is for general information purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information in this article may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information in this article is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance.

Any projections contained in this article are predictive and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.