Have the global tech giants passed their peak?

Update – 15 October 2018: The following article was initially published on 21 September, based on prevailing valuations, to outline our thoughts on the inherent risks for FAANG stocks. This cohort have subsequently experienced significant share price declines in October after broader market sentiment particularly towards the US technology sector turned negative. On the surface our article may appear prophetic, however we don’t see the recent correction as a reflection of the key risks highlighted in this article these are yet to be acted on by the market. Regardless of whether the FAANGs decline further or even recover from this point, our fundamental reasons for not investing in Facebook, Apple, Amazon and Netflix remain unchanged. Similarly, our rationale for investing in the owner of Google remains valid and is in line with our long term approach to investing.

Many people love an acronym these days and fund managers are no exception so we’ll start this article with a somewhat cryptic collection of terms. The reference to FAANG stocks has been gaining broader recognition as a result of the meteoric rise in the share prices of its constituents. In 2018 this dynamic has led to a situation where the FAANGs have often determined the direction of the US S&P500 stock index. As with any stock, the higher the share price rises, the greater the risk of a correction, but we believe the inherent risks for some FAANG stocks are much deeper.

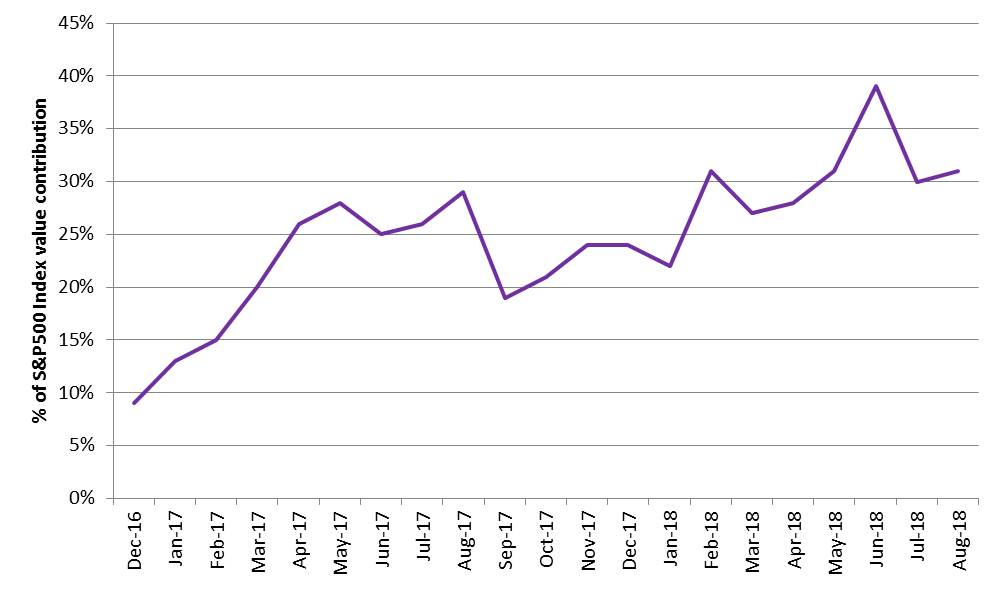

The collective of mega-cap global consumer technology companies known as FAANG stocks — Facebook, Apple, Amazon, Netflix and Alphabet’s Google — have rapidly grown in value over the past two years as a result of success in global penetration of their consumer products and platforms. These five stocks have become increasingly integral to the broader market’s performance and now represent around 15% of the S&P500 by weight. Their growing concentration within the US market has meant they account for 20-30% of the market’s movement in value. Expressed another way, for the first half of 2018, the positive return for the S&P500 was due to the FAANGs as they collectively added more than twice the value that the rest of the market lost. The growth in passive index tracking products also contributes to this self-fulfilling cycle, where price rises lead to index weight increases which then push prices further. Both Apple and Amazon reached milestones of US$ 1 trillion in total market value this year and are now larger than the annual output (GDP) of some countries such as Switzerland, Saudi Arabia and The Netherlands.

12 month rolling percentage of S&P valuation created by the FAANGs

Source: Pendal, Bloomberg

For simplicity we’ll continue to use the FAANG abbreviation to represent this group of five leaders in global technology enablement as we address a pertinent question on the minds of many onlookers: Could the Fear Of Missing Out on the massive share price gains become the more satisfying notion of Lucky To Miss Out? There are a number of valid reasons why at the present time, would-be investors in FAANGs can afford to be more sanguine about avoiding these stocks.

FAANGs reached their peak valuation in June before the market was made aware of earnings disappointments from Netflix and Facebook. Netflix’s share price was down 14% for the month; Facebook’s shares declined 20%, or US$ 120 billion to represent its largest one-day loss in value. This was a strong market reaction to the company’s future earnings prospects and the concerns are legitimate. Facebook’s core product is mature and revenue growth is primarily based on increasing prices for advertising. Netflix is now basing its expectations on user growth rates with little consideration for the incremental cash it will generate from each subscriber.

Similar concerns exist for other stocks in this group. Amazon’s business model is all about growing their share of online retailing with a focus on generating revenues rather than profits. At some point one will have to justify the other. Apple has a somewhat similar approach to capturing the biggest slice of the mobile device market. Its unit sales haven’t grown over the past two years and despite claims of its customers being captive to Apple’s iOS ecosystem, its market share has actually declined. And while Google has grown its share of the competing Android platform, it is heavy exposed to the highly cyclical online advertising market.

While these factors don’t necessarily mean these are bad companies they do increase the downside risk if current strategies fail to deliver. We would argue this is more than a remote possibility, considering the rapidly advancing intersection between technology, competition and fickle consumer preferences which can abruptly impact revenues.

Regulators on the trail

Until recently, FAANGs have been fortunate to grow while being relatively unfettered by government controls. Effective control over these behemoths of the technology world is far from simple to achieve, but the renewed vigour of regulators together with the rise of populism and anti-establishment political forces now present as a sizeable risk to the FAANGs’ business models, pricing structures and market access. Consider Facebook and its unintended leakage of personal information to Cambridge Analytica. This not only drew the ire of its millions of users but also resulted in CEO Mark Zuckerberg being hauled in for a ‘please explain’ grilling by US Congress. At the hearing he argued Facebook is a technology platform rather than a media company, although he conceded Facebook is responsible for what is posted on its platforms. This is an important distinction in the US as media companies face stricter regulations, are legally responsible for the content they publish and can be sued over the content of their platforms.

Zuckerberg sees greater investment in artificial intelligence as part of the solution but he knows there is some way to go on that front. Facebook have committed to hiring 10,000 new cybersecurity and content monitoring employees by the end of 2018. But of even greater concern is the broader impact of content restrictions. Facebook’s engagement metrics are most valuable at the extremes of content, so any material restrictions on content will have direct implications for advertising revenues. The US currently lacks a single comprehensive law regulating the collection and use of personal data, but the tide against the capitalism supports for mega companies like Facebook cannot be ignored. Recall the US Department of Justice case against Microsoft in the late 90s when the regulator sought to break up Microsoft on anti-trust law violations. Microsoft retained its structure on appeal, but it did result in the death of Netscape and subsequent ascension of Google.

Being a global platform also means offshore regulators share an interest. In July the European Union regulatory authority fined Google €4.3b (A$6.9b) for abusing Android’s monopoly to push Google’s apps on its own platform. The ruling determined that Google forced phone makers to preinstall its Chrome browser as a condition for accessing the GooglePlay app store and illegally paid manufacturers to preinstall its search app exclusively. Google are now required to give manufactures and phone providers free choice on the apps they install.

Margrethe Vestager, the European Commissioner for Competition, has been busy over the past few years increasing her efforts to limit the commercial power held by these companies. It makes sense that Europe rather than the US take the lead as it assumes all of the downside from social issues, interference with elections, job destruction, tax avoidance and anti-competitive behaviour but little of the upside from high-paying jobs, donations and value creation. The General Data Protection Regulation (GDPR) which came into effect in May is the most stringent legislation to date and aims to provide more control to citizens over their personal data. While it is still early to assess the real impact from GDPR, the cynic in me thought the timing of Facebook’s downgrade on their second-quarter earnings was interesting.

A little more than luck at stake

We acknowledge these are great companies, leading in their field with a global footprint. But everything has a price and as stewards of our clients’ capital we are reticent to invest on the basis of market leadership alone. Our process involves buying leading companies which have fallen out of favour with the market, often for reasons external to their underlying operations. They must be leaders in their industry but must also be attractive in terms of free cash flow, dividend yield, and trade on a buyout ratio of at least 8%. Our analysis needs to identify a clear catalyst for higher earnings. On these factors, Google (Alphabet Inc) is the only FAANG that qualifies for investment.

Google operates a robust business model with a 90% share of online search, 70% share of the mobile operating system (Android) and 45% of the online advertising market. YouTube is a clear leader in video and becoming a meaningful grow driver for the group. The regulatory risk for Google is considerably lower than for other FAANG stocks.

The only conceivable regulatory action that would have a meaningful impact on Google would be for its search algorithms to essentially become a utility where by the market is granted access under a regulated fee and licensing regime. We don’t view the likelihood of this happening any time in the foreseeable future as very high. The great advantage of Google’s search product is that it ages in reverse its algorithms become more powerful the more they are used. It also operates in a duopoly as online advertisers are effectively limited to two platform choices. Facebook and Google together account for about 80% of the global (ex-China) online advertising market.

The stock trades on a 16x earnings valuation multiple (excluding cash and losses from its non-core business) which is reasonable even after considering the risks. This collection of businesses is expected to generate earnings growth in the mid-teens for the current fiscal year.

By comparison, Amazon trades on a valuation that is very hard to justify. If we separate Amazon’s two core business Amazon Web Services and Marketplaces and value them separately, in order to justify Amazon’s current valuation our analysis concludes that the Marketplace business would need to achieve a 15% earnings margin. That margin would be three times larger than the best food retailers have ever managed to sustain in one of the most competitive and price sensitive industries in the world.

As for the other FAANGs we don’t see their current valuations as justified on the measures we focus on. We also believe the risks to their future earnings from regulatory imposts are yet to be appreciated by the market. Cyclical and product specific factors also arise when considering the maturity of some business lines. Market momentum factors may act to support their share prices in the short term, but at prevailing valuations I prefer to remain a humble user of iOS, transact via EFT, stream VOD and PM my contacts without sharing the nascent, yet real risks as a shareholder.

This article has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and the information contained within is current as at October 9, 2018. It is not to be published, or otherwise made available to any person other than the party to whom it is provided.

PFSL is the responsible entity and issuer of units in the Pendal Concentrated Global Share Fund (Fund) ARSN: 613 608 085. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1800 813 886 or visiting www.pendalgroup.com. You should obtain and consider the PDS before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This article is for general information purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information in this article may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information in this article is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance.

Any projections contained in this article are predictive and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.