South Korea and Malaysia in focus

Histrionics – of or belonging to stage players or to play-acting; theatrical; dramatic.

This month during summer break I spent some time on the East Coast of the US. It was surreal listening to family and friends separated by a chasm on their political views. But it was also amusing to be part of the conversation fed by the daily drama emerging from the White House. More so as for the first time Americans wanted to know what Asia in general thought about President Trump and his administration. Fortunately, we’ve had our fair share of colourful leaders in Asia. Over the years, experience has inured us to recognise that political developments can make a difference to broad market movements. What is of more relevance, though, is the trend of the US dollar, which still remains the reserve currency. Look no further than the South Korean market this year. A belligerent North Korea, an impeached and deposed President, management of its largest conglomerate, Samsung Electronics, accused of involvement in money politics, and China threatening retaliation for siding with the US, who would have expected South Korea to be amongst the best-performing markets in the region over the year to date?

Korean stocks boom as the US dollar swoons

More in Malaysia

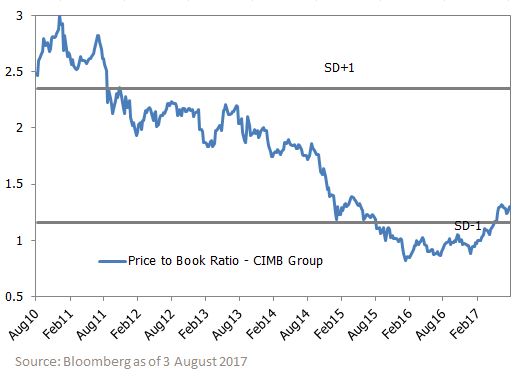

Our exposure to Malaysian stocks has risen to 5%, from a zero weighting at the start of the year. Generally speaking, analysts and commentators alike rarely have much to say that is complimentary on the way the Malaysian economy is managed. I, too, am sympathetic to that viewpoint. However, when deterioration in economic conditions has been reflected in market prices, both in equities and the currency, it does make sense, in my view, to take a positive view. There is no other justification except to say that a lot of the negativity is in the price, and I don’t think we will lose too much on our Malaysian investments. But the probability that things can go right is, I believe, high and time will tell how well that scenario develops.

Malaysian bank CIMB Group looks cheap on a price-to-book value basis

This article has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and the information contained within is current as at August 11, 2017. It is not to be published, or otherwise made available to any person other than the party to whom it is provided.

PFSL is the responsible entity and issuer of units in the BT Wholesale Asian Share Fund (Fund) ARSN: 087 593 468. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1800 813 886 or visiting www.pendalgroup.com. You should obtain and consider the PDS before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This article is for general information purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information in this article may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information in this article is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Any projections contained in this article are predictive and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.