Santa says “conditions too toxic” for his annual rally

Oxford Dictionaries, the world’s leading authority on English linguistics, has judged the word ‘toxic’ to best “reflect the ethos, mood, or preoccupations of the passing year”. It’s an appropriate word to describe many of the alarming developments across the world – and their impact on investment markets. With the S&P500 down over 5% so far in December, the seasonal phenomenon of a ‘Santa rally’ – which has prevailed in 64 of the 89 December periods since 1929 – looks set to be an anomaly in 2018.

The story of 2018

After a reasonably strong January effect – another well-observed phenomenon of general optimism on stock markets to commence the year – positive sentiment quickly gave way in February to concerns over inflation coming back with a vengeance, coupled with aggressive monetary tightening which sent the US stock market to a 10% correction. Other developed and emerging markets followed to varying degrees before a relatively stable period ensued. October came and volatility returned, US treasury yields peaked and bellwether commodities including crude oil and iron ore fell prey to sellers.

Naturally, the story of 2018 goes much deeper, with multiple dynamics at play across asset classes and industries. In this article we delve into the minds of Pendal’s portfolio managers to attain their thoughts on the year, and more importantly, insights into what investors need to be aware of for 2019 and beyond.

Australian Equities

The Australian share market has experienced its most volatile year for some time. The correction we saw in February was followed by a reasonable recovery from March through to August, pushing the S&P/ASX 200 back above the 6000 mark, only to decline again in September. The market has de-rated to its longer term average price-earnings valuation of 14 times, with many good companies trading now below that level. Crispin Murray, Head of Equities, has regularly spoken about the need to focus on company fundamentals to identify catalysts for re-rating. With the market’s growing divergence we posed a few key questions to Crispin.

Q. How are you viewing the market’s recent action?

A. 2018 has ended on a note of increased volatility, with the subsequent de-rating driven by fears over the potential impact of global monetary tightening and trade wars on economic growth. This has weighed particularly on cyclicals and growth names. However, data indicates that the underlying US economy remains robust and domestic earnings estimates are not showing material deterioration. We have been using the recent weakness as an opportunity to buy some new positions and add to some existing ones. But we are being judicious as growth and defensives are still looking expensive versus the rest of the market and their own history.

Q. Much of the market’s macroeconomic concern is focused on China. What is your high-level outlook here?

A. Economic growth in China remains a key factor for commodity prices and therefore prospects for the Australian mining sector in 2019. Growth has been decelerating on the tightened credit that came with the Government’s clamp down on the shadow banking sector. Markets fear this will see a significant decline for demand for commodities, particularly if exacerbated by ongoing trade frictions. While this is a risk, we need to remain mindful that supply-side discipline remains supportive for commodity priced and China would probably move to stimulate an overly weak economy and not sit idle.

Australian miners remain cash generative and disciplined in their capital allocation. We remain cautious in the near term given the risks but are keeping a close eye on the sector, ready to take advantage if we see sentiment turn too negative. In the interim, we have been building a position in mining services as we reach that point in the cycle where miners need to replace and expand mines and maintain their equipment.

Q. You have been talking about corporate disruption for the past two years, does this trend continue into 2019?

A. Several sectors of the economy and market continue to face challenges to traditional business models and industry structures from technology, competition, and government/regulatory intervention. It is the latter which is looking likely to shape up as the key disruptive element in 2019. Not only do we have the Royal Commission final report due in February, but in recent weeks APRA’s action on IOOF and the ACCC’s initial response to the TPG/Vodafone deal suggests regulators will be increasingly inclined to flex their muscles. Banks, wealth management and power generation have all been hit hard by government intervention in 2018. There are signs that both insurance and aged care may be under scrutiny in 2019, however we would not be surprised to see the effects of this trend manifest in other parts of the economy. As with all disruptive forces, this can provide a challenge for companies – but also opportunities for active investors as heightened uncertainty leads to the chance of mis-pricing risk.

Fixed Interest & Cash

Over the year, Australian bond yields were relatively range-bound and the yield curve flattened in sympathy with its global peers. This was alongside swings in risk sentiment that revolved around geopolitical risks, with changes in US Federal Reserve (Fed) and European Central Bank (ECB) policy expectations also playing a part. Following the latest rate hike by the Fed in December and a tempering of market expectations for further hikes in 2019, we asked Vimal Gor, Pendal’s Head of Bonds, Income and Defensive Strategies for his thoughts on how rates and credit are likely to play out.

Q. Australian bond yields have traded lower this year, while US bond yields look set to finish 2018 higher. Is this divergence expected to continue in the period ahead?

A. There are two forces that should continue to direct US yields in 2019. The first is the outlook for the US economy. We believe the US is still mid-cycle and has the potential to remain relatively strong in the near-term. This is reflected in leading indicators like manufacturing surveys. While this would point to higher yields, the Fed has also acknowledged that rates are now closer to their neutral level and expectations for hikes next year have moderated significantly. As such, the potential for yields to increase may be limited.

The second force remains risk appetite, where an increase in broader market volatility and geopolitical concerns could put pressure on yields. Australian yields should take some guidance from the US, but our view that the RBA will remain on hold for at least the next year will likely see them remain range-bound and below their US counterparts.

Q. The ECB recently announced the end of its quantitative easing program. Do you see them raising rates in 2019?

A. We believe the ECB will not raise rates in 2019, which has been a non-consensus call until recently. Economic activity for several of the Eurozone’s largest members has deteriorated this year including Germany, France and Italy. Additionally, all three will face political uncertainty that may compound over the next year. Italy will also face fiscal constraints, which maybe a drag on economic growth and could cause GDP to contract further. At the same time, the end of the ECB’s asset purchases will remove a degree of support for both sovereign and corporate bonds in the region, which supports our negative bias for European credit and the euro.

Q. Is market volatility expected to rise, fall or do both, and how does volatility impact your investment strategies?

A. The ongoing liquidity withdrawal from the global financial system points to higher volatility going forward compared with previous years. Globally, central bank balance sheets will shrink for the first time in a generation. With tighter availability of credit comes more stringent pricing of risk. It also brings a less-forgiving market as illustrated by the reaction to bouts of geopolitical uncertainty over the year. We expect such an environment to persist in 2019 and our funds are positioned to benefit accordingly.

Global Equities

As expected, market volatility increased this year in response to largely macro and geopolitical issues. Prime among these were Trump’s policy agenda, US-China trade, Brexit machinations and monetary tightening. We also saw significant sector rotation as Financials rallied on expectations of aggressive Fed tightening before reversing late in the year. The US technology heavyweights – Facebook, Apple, Amazon, Netflix and Google’s parent entity Alphabet – or ‘FAANG’ stocks, were key drivers of the market’s gains during the first half before suffering a reversal when softer earnings expectations spooked the market. Ashley Pittard, Portfolio Manager of the Pendal Concentrated Global Share Fund, lends his insights into how the team navigated the year.

Q. You have not invested in FAANGs this year aside from Google and remain positioned that way. What is the team’s rationale for this position?

A. Our discipline of buying high quality, industry leaders that meet our valuation hurdles led us to steer clear of the FAANGs except Google. There is no dispute they are great companies operating world-leading platforms and product suites, but their valuations left little to gain and importantly, some of these names carry nascent regulatory risks. We wrote about this at length earlier in the year when we saw better value in other areas of the US tech sector such as semiconductor manufacturers like Analog Devices and Texas Instruments.

Q. How were you positioned in financials?

A. Based on our expectations of rising interest rates in the US and monetary tightening elsewhere, we saw great potential in operators of stock exchanges. There are listed companies like CME Group, Deutsche Boerse and Japan Exchange Group which are direct beneficiaries of higher market volatility and therefore, higher trading volumes. These companies delivered impressive returns for our clients this year of around 41%, 20% and 15%, respectively.

Q. Given stock exchanges and semiconductor names have done well this year, what areas do you expect to find interest in 2019?

A. We’re long term investors and rely on our valuation discipline to guide our research focus. The stock exchange and semiconductor names above are great businesses and remain attractive based on our metrics. The heavy macro influences this year have driven the share prices of some great industry leaders to attractive levels and we’re closely monitoring companies within the infrastructure, pharmaceuticals and consumer-related industries and expect to see additions next year. During the year we reduced our technology weight in the Fund from 20% to around 12% and increased the exposure to pharmaceuticals to 11%. We’ve also held a higher level of cash over the past few months (up to 11%) and we expect to reinvest as opportunities arise.

Listed Property

The A-REIT market has delivered a positive return for the year to date, surpassing the negative returns from share markets in Australia and around the globe. We asked Pete Davidson, Head of Listed Property at Pendal for his thoughts on the sector.

Q. What’s driven A-REIT returns this year?

A. We’ve seen four main themes driving returns for the listed property sector in Australia:

1. lower Australian bond yields

2. limited new equity issuance

3. some merger and acquisition activity; and

4. very strong office and industrial markets.

Lower Australian bond yields reflect the fact that after 27 years of uninterrupted growth, the Australian economy is slowing. Our economic growth rate is now below the US for the first time ever, with Australian bond yields around 0.40% below the equivalent US bond yield.

A-REITs are very sensitive to Australian bond yield movements, so lower bond yields have served to underpin A-REIT valuations. Equally, slowing economic growth has encouraged many investors to rotate back to defensive asset classes such as A-REITs over the course of 2018.

Another factor is simple supply and demand. The table below highlights just how little fresh or new equity has been raised this year. Low capital raisings translates into good demand for existing assets.

A-REIT capital raisings

Q. It was a big year for property portfolio M&A activity. Where was the appetite and what was the impact?

A. We’ve seen significant corporate merger and acquisition activity in A-REITs this year, much of it acting as equity withdrawals. Notable takeovers included Investa Office, Gateway Lifestyle, Propertylink and the gargantuan takeover of Westfield – the largest takeover in Australian corporate history. Looking forward to next year there is likely to be further activity in the market.

The direct commercial property market was strong in 2018. Bidding activity for Investa Office (two direct investors competing to buy a $4b premium office portfolio) highlights strong demand for office assets. Equally, investors are keen to buy logistics and industrial assets. In 2018 we saw competing bids for Propertylink, an industrial A-REIT, while Goodman Group, a global logistics owner, was the best performing A-REIT over calendar 2018. The rising asset values in the office and logistics sectors helped to underpin returns for A-REIT investors.

Looking ahead, a delicate balance of the above forces should help underpin the sector’s outlook for 2019.

Emerging Market Equities

2018 has been a difficult year for emerging markets (EM), as a challenging global environment has coincided with some country-specific challenges to see weakness in both equities and currencies. James Syme, Portfolio Manager of the Pendal Global Emerging Markets Opportunities Fund recently visited Australia to provide some perspective on developments this year.

Q. After a tumultuous year for the asset class, what can we expect to see in 2019?

A. The external environment is likely to remain difficult, but one legacy of 2018 has been the extremely attractive valuations appearing in parts of the EM equities universe, particularly within those countries reliant on domestic demand. The MSCI Emerging Markets Index is cheap relative to its history, despite the rise of the (comparatively expensive) internet sector in the index. Many parts of the asset class now trade at single-digit forward price/earnings ratios. We believe there is substantial opportunity in the asset class, but there will need to be an improvement in the external environment before that opportunity can be realised. Overall, we are very positive on the outlook for emerging market equities in 2019. We feel the current negativity towards the asset class is unwarranted, although gains may be loaded into the back-end of the year.

Read more of James’s 2018 review of emerging markets

Multi Asset

Considering all the challenges in 2018 we asked Michael Blayney, Pendal’s Head of Multi Asset, to makes some observations with a longer term context.

Q. How have the dislocations in markets this year affected your return expectations for diversified funds?

A. Rather than dislocations, we see the market gyrations this year as more of a return to normal conditions after nearly a decade of artificially low volatility. It is our view that central bank support for markets since the GFC has led to unusually-low realised volatility since the start of Quantitative Easing in 2009. As central banks reverse this policy, we see the potential for markets to return to their core function of price discovery in order to facilitate the efficient allocation of capital. This is a good thing.

Our assumptions have changed somewhat in response to recent market declines: for Australian equities our long-term return forecast has increased to 8.75% pa, up from 8.25% a year ago. Interestingly, market moves of around 10% that we’ve seen this year don’t change the long-term expected return by as much as might be expected. Let’s say your investment horizon is 10 years and your expected return for a given investment over that time is 8% pa. If the market price of that investment falls by 10% then your expected return rises to only 9.1%, all other things being equal. If your investment horizon is 30 years then the expected return increases to only 8.4%. Hence, moves of the magnitude we’re seeing are more noise than a valuable signal in the context of long-term wealth creation. Of greater importance is to ensure that you’re invested in the right asset mix and risk profile so that you can both handle inevitable declines in market prices as well as growing an adequate nest egg over the long-run.

What the current situation (ie more extreme market movements combined with a move towards markets functioning more normally after a decade of central bank intervention) provides is the potential to increase returns via active management. To provide an example, during November our dynamic asset allocation (DAA) process identified US large-cap equities as being sufficiently expensive to warrant an underweight over the medium-term (1-5 years) while Korean equities are cheap enough to justify an overweight over a similar investment horizon. The respective entry points for these portfolio tilts create an attractively-skewed distribution of future returns, giving the high probability of adding value. US equities have subsequently fallen further than Korean equities, thereby generating a positive active return for investors in a number of Pendal’s actively managed multi asset products. We view several other equity markets in Asia as being modestly cheap, but not yet cheap enough that the probabilities are sufficiently compelling.

Q. The average super fund has delivered annual returns of 7-8%pa over the past few years. Are these returns achievable in the current environment?

A. I would expect passively managed balanced funds to struggle to meet these return targets. The reasons here are fairly intuitive. Consider the forecast return for the strategic asset allocation (SAA) of the Pendal Active Balanced Fund which is around 6.5% (comprised essentially of CPI+4 to 4.5%), with the balance of the return contribution sourced from active management and risk reduction. Through this approach, total gross returns of 7-8% are theoretically achievable. For the average passive balanced fund which is essentially premised on no contribution from actively selecting investments and managing risks, the likely returns would be closer to the 6 to 6.5% mark, before fees.

For further insights from Pendal’s portfolio managers please visit the education & resources section of our website.

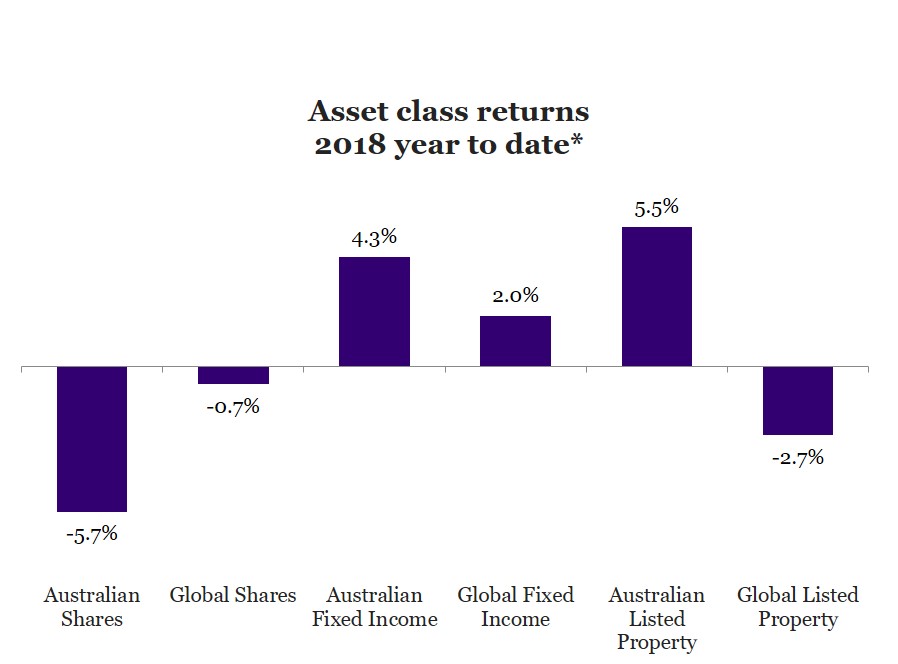

* Asset class returns are based on appropriate index returns for the calendar year to 20 December 2018. Australian shares: S&P/ASX 300 Accumulation index; Global shares: MSCI World ex Australia Total Return (AUD) index; Australian fixed income: Bloomberg AusBond Composite (0+yr) index; Global fixed income: JP Morgan GBI Global Traded A$ Hedged index; Australian Listed Property: S&P/ASX 200 A-REIT Accumulation Index; Global Listed Property: FTSE EPRA/NAREIT Developed ex Australia (A$ hedged) Total Return Index.

This article has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and the information contained within is current as at December 21, 2019. It is not to be published, or otherwise made available to any person other than the party to whom it is provided.

This article is for general information purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information in this article may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information in this article is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Any projections contained in this article are predictive and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.