Crispin Murray: what’s driving ASX stocks this week

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

MARKETS continued to grind higher on limited news flow last week.

Improved sentiment on global growth pushed the energy sector ahead 8.5%, which led the S&P/ASX 300 to a 1.6% gain for the week.

There were several factors at play, including a sense that the worst overseas Covid outbreaks are coming under control. There are indications Europe will soon follow the US into a broader re-opening.

OPEC’s meeting was very short, signalling that its stance of restricted supply remains firm. Brent Crude rose 2.8%.

Covid and vaccines

Global cases continue to trend in the right direction in the US and EU — as well as some of the worst-hit countries such as India. Continued vaccine exports to under-supplied countries is boosting confidence.

US mobility levels have now passed pre-COVID highs. The EU is trending higher, which is helping improve sentiment on oil.

Economics and policy

US non-farm payroll data showed an additional 559,000 new jobs in May. This was better than April, but was still well below the jobs growth that many expected with the recovery.

There are still 7.6 million fewer jobs than before the pandemic. There is a view that on-going federal unemployment insurance top-up payments are discouraging people from job hunting. These payments are due to roll off in September.

A buffer of excess savings accumulated in the past year is also likely to be playing a role. The result is a falling workforce participation rate at a time of huge jobs supply.

Leisure and hospitality account for about 40% of the gap in jobs compared to pre-Covid. Education and health make up another 15% or so.

Wages are a big focus given latent concerns on inflation and people’s reluctance to return to work. Wages grew faster than expected in the latest data. But the year-on-year rate is still subdued at 2% growth.

The composition of wage growth is distorting headline figures to a degree. We have seen a faster return in lower-paid jobs which is depressing the headline figure.

Interestingly, leisure and hospitality is bucking this trend, with 8.8% wage growth. This highlights labour supply issues in the sector.

The debate is whether labour supply issues will be resolved relatively quickly or whether this will seed wider spread inflation.

Another point to note is that productivity is high.

The US has returned to pre-Covid GDP — with far fewer workers. This clear gain in productivity reduces the importance of unit labour costs.

These issues will play into the Fed’s policy deliberations. At this point most expect the Fed to start talking about tapering in the June meeting, without drawing any firm conclusions. The focus is on clear signalling to avoid a “taper tantrum” in markets.

We won’t return to the trend of long-term job growth until mid-2023 based on the current jobs growth rate. This is consistent with the Fed’s message of no rate tightening for two-to-three years.

This helps explain why bond markets have so far seemed comfortable with the Fed’s stance — and the benign reaction to signals around tapering.

This is supportive for equity markets, as is the ongoing growth pulse.

The US Composite Purchasing Manager’s Index (PMI) is well above its highest level in over a decade. The Global Composite PMI, while trending upward, is still below its highs.

There is scope for the Global PMI to follow the US, emphasising that there are several legs to the global recovery story. This can prolong it further than many are expecting.

Markets

Bonds remained largely unmoved last week and the broad environment was reasonably benign.

There was some movement in the commodity space. Brent crude rose 2.4%, passing a technical level that suggests it could head towards US$80. If that’s the case, it will be interesting to see what this means for bonds.

Elsewhere iron ore rose 10.8%. Copper and gold consolidated.

Overseas we started seeing gains in the Real Estate Investment Trust (REIT) sector, which has long languished. The main explanation is that it is a later cycle play on the re-opening.

In Australia the Energy sector rose 8.5% — though it’s still up only 6.8% for 2021 so far. REITs rose 2.6% domestically, but are also lagging for over the year to date (up just 6.4%).

Financials remain very consistent, up 1.6% for the week. There are some early signs of rotation from the banks (which are up 30.2% for the year to date) to the insurers.

Utilities (+5.8%) gained some respite, reflecting the local issue of higher power prices following a recent explosion at the Queensland coal-fired Callide Power Station.

Six of last week’s eight top performers in the S&P/ASX 100 were energy stocks. Origin (ORG, +15.7%) led the pack, a beneficiary of higher oil and power prices. Santos (STO) was up 12.2% and Oil Search (OSH) gained 11%.

Worley (WOR, +15.6%) had a fortuitously-timed investor day, which played to the theme of a rising oil price driving a recovery in capex in the sector. We are mindful that part of the reason oil is strengthening is a lack of new investment response.

The iron ore miners did not respond to the 10% gain in prices. This reflects some scepticism around the sustainability of price drivers, which is linked to the stimulus and economic recovery.

In contrast, sentiment remains bullish on the copper miners despite a 4.5% drop in the price last week. This is regarded as a longer-term theme related to renewable energy and electric vehicles.

Tech was the week’s loser, for no discernible reason. Appen (APX, -8.7%) was the worst performer. Altium (ALU, -3.5%) was also weak. There are signs of a base building in tech stocks in the US, although we do not expect sustained market leadership given the broader macro backdrop.

Gold stocks reflected the yellow metal’s 1.6% fall. Evolution (EVN) fell 4.9% and Northern Star (NST) was down 4.6%. We see the gold price as well supported.

About Crispin Murray and Pendal Focus Australian Share Fund

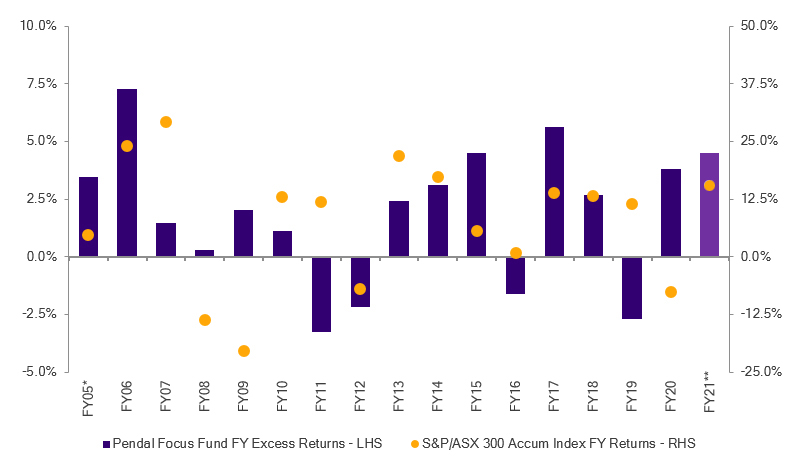

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 30 Apr 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management. Find out more about Pendal Focus Australian Share Fund here. Contact a Pendal key account manager here.

This article has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and the information contained within is current as at June 7, 2021. It is not to be published, or otherwise made available to any person other than the party to whom it is provided.

PFSL is the responsible entity and issuer of units in the Pendal Focus Australian Share Fund (Fund) ARSN: 113 232 812. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1800 813 886 or visiting www.pendalgroup.com. You should obtain and consider the PDS before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This article is for general information purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information in this article may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information in this article is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance.

Any projections contained in this article are predictive and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.