Global equity investors need a new mindset for the 2020s

Ashley Pittard, Head of Global Equities at Pendal recently presented his thoughts on the extent of risk that has developed in global equity markets at the Portfolio Construction Forum’s Strategies Conference 2019 – “20/20 Vision” . This article outlines the insights shared around why investors need to adopt a different mindset when it comes to investing in global equities in the 2020s.

Today global equities investors are facing into markets where the risks go well beyond trade wars and currency tantrums.

I’m proud of the first quartile performance Pendal’s Concentrated Global Share Fund has achieved since we commenced.

But it’s now more important than ever for investment managers in the global equities sector to have the right active strategy for the 2020s.

The extreme risk in global equities right now requires a different mindset as we enter the new decade.

September 15 marks the 11th anniversary of the Lehman bankruptcy and Global Financial Crisis (GFC).

That event sparked one of the greatest credit and equity bull markets in history as central banks adopted extreme and unprecedented monetary policies.

Along with conventional monetary policy actions including 735 interest rate cuts around the world, central banks took unconventional actions such as $US13 trillion worth of quantitative easing which essentially refers to “printing money”, preventing debt default and deflation.

End of the post-GFC era

Over the past ten years broad investment in global equities has been a great investment decision.

Investing in an index fund, exchange traded fund or a growth theme such as tech stocks would have done very well for your retirement savings instead of holding money in the bank.

After the GFC investors benefited from tail winds that drove share prices higher – such as falling interest rates, lower volatility, a declining Australian dollar and quantitative easing.

But that’s now changing.

The 2020s will be very different to the past decade.

In the new environment investors will need to be very selective rather than pursuing broad market exposure for their portfolios.

Macro supports such as cheap money and big government balance sheets won’t provide a blanket for all listed companies.

At Pendal we are contrarian, long-term fundamental stock pickers when it comes to global equities — so this environment plays to our strengths.

Markets in the new phase

Why am I so confident that these 10-year tail winds will become headwinds – even when volatility measures suggest risk is low in global equities?

It’s a hard ask for market valuations to be compelling when the market is trading at all-time highs. Price-to-Earnings ratios are over 17x and the S&P500 Index has grown to nearly four times its value since its GFC lows.

Bifurcation in the market is extreme and distortions are occurring within equity markets. We have a handful of mega cap technology-related stocks that have carried the market higher, while at the other end of the spectrum sectors deemed to be eternally disrupted have languished.

Growth sectors are significantly over-valued on traditional historical measures while value sectors are shunned.

This year just 6 % of the MSCI World Index stocks have accounted for 53% of the return for the global equity index.

Meanwhile, interest rates are down a long way. We have had 29 cuts from central banks in 2019 and government bond yields for the largest economies are at a 120-year low.

It is hard to say they will be going significantly lower. Consider the US 10-year bond as a proxy. In 2012 when the market believed the euro would break up and European banks would be nationalised, the US 10-year bond touched 1.36%. In 2016 when the ‘Brexit’ vote occurred, it touched 1.36%. In August it has drifted past the 1.75% level.

The Aussie dollar has collapsed from $1.10 over the last decade to hover around the US$0.70 level within a small range. Currency volatility for the major economies is at the lowest level since 1992.

But we have just started to see the US officially label China a currency manipulator.

It is timely to recall the 1995 Plaza Accord, a joint-agreement between France, West Germany, Japan, the United States and the United Kingdom, to depreciate the US dollar in relation to the

Japanese yen and German Deutsche Mark by intervening in currency markets. This event turned currencies upside down at the time and placed Japan into its lost decade. This event turned currencies upside down at the time and placed Japan into its lost decade.

It’s interesting that many economists saw this accord as a direct response from the US to the threat from Japan’s growing status as an economic superpower.

In my view equity risk is the highest in more than 20 years – regardless of what traditional volatility measures suggest.

When you have $US13.7 trillion of negative yielding debt globally investors have been pushed up the risk curve to chase ever decreasing yields.

And when you fundamentally change the value of cash massive distortions occur. We are seeing this on many levels.

Global debt is now 3.2 times the size of global GDP – again at an all-time high.

We have been here before

The tech sector – especially the FAANGs (Facebook, Amazon, Apple, Netflix and Google)- have been the darlings of the bull market for the last 10 years.

Real estate and utilities stocks have also been drivers of market returns, thanks largely to declining interest rates.

But the elephant in the room is the tech sector.

It has tripled its index weight since the GFC and doubled its index weight in the US market over the past five years.

Tech has been at the epicentre of this self-fulfilling circle — declining interest rates, exploding debt and rampant passive investing have helped to triple its representation of the market.

No doubt these are great businesses but it’s amazing how big their market capitalisations are — especially when compared to the GDP of some countries.

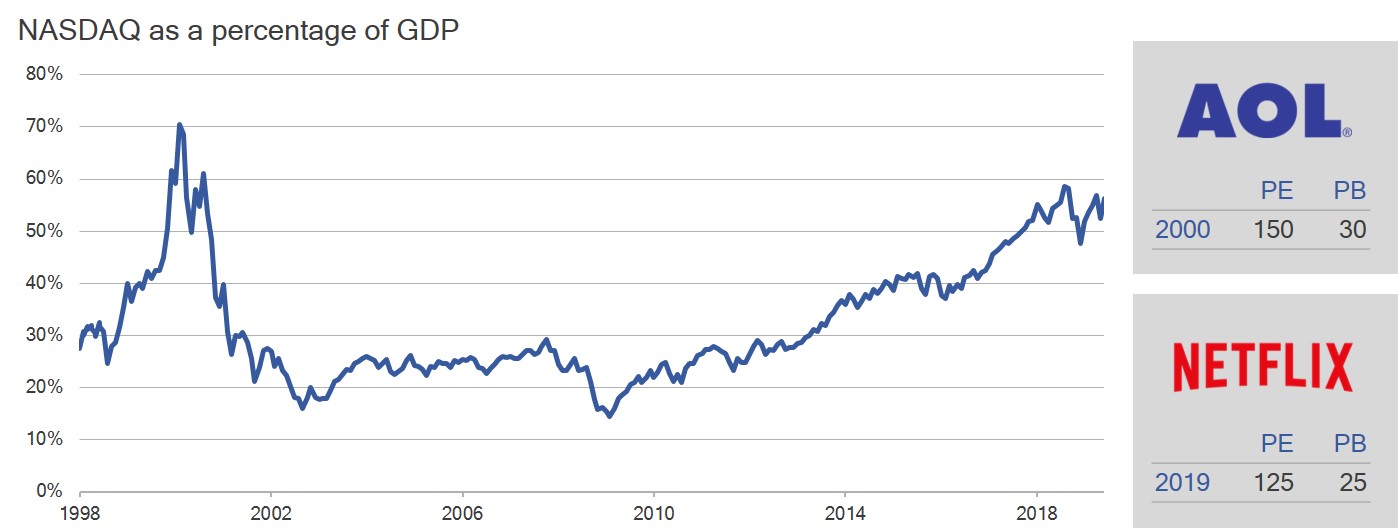

If we use the 2000 technology bubble as another proof point, the valuations again are stark.

It’s uncanny how AOL at its peak traded at similar levels to Netflix today.

Look at the metrics on the right hand side of this graph:

* Source: Bloomberg, Pendal. PE refers to price-earnings ratio, PB refers to price-book ratio.

You could argue about the relevance of using a price-book ratio for these tech names but as a long term valuation tool across different sectors, price-book is still a clean gauge of value.

And Nasdaq as a percentage of GDP is near historical bubble levels.

The extreme size of valuation premiums is a key risk driver.

Passively fulfilling a virtuous cycle

Here’s another aspect of the self-fulfilling circle. Passive and index-hugging strategies are reinforcing these valuation trends.

Over the past 10 years $US4.1 trillion has gone into passive investment funds versus outflows of $US1.5 trillion out of active.

In the year-to-date we have seen 65% of stocks in the MSCI World proceed into bear markets as passive inflows top $US7.4 billion and outflows from active strategies top $US22.4 billion.

The issue here is index and traditional strategies — by their inherent design — see more and more investors bet on higher growth for what has already risen.

This creates distortions in the market as passive ETFs focus on the largest companies in a sector, not the best companies.

Why we’re different

At Pendal, we are clearly very different.

We don’t look at the largest companies — just the best companies.

We focus on leading number one or number two franchises in their space when they are out of favour — regardless of size.

That is the lowest cost producer if it’s a commodity or largest market share if it’s a bank. We like monopoly assets.

We look at industries horizontally — not vertically as do many traditional index strategies.

We focus on fewer higher quality businesses and build a deep understanding of them like a business owner would.

We launched our Concentrated Global Share Fund three years ago and we have been very happy with the 1st quartile performance over the three-year period which reflects this very different approach compared to passive index following strategies.

Our philosophy and process has been the same since I started at BT Australia (the former entity name of Pendal) more than 20 years ago.

We have a universe of about 500 leading businesses that we follow.

We spend a lot of time focusing on disruption in industries. Usually we are buying businesses when we think they are cyclically depressed — while the market may think they are structurally impaired.

In our experience, only 15-20% of the market is attractive at any point in time.

You need to be very selective to grow wealth over the long term. Our top 10 holdings (see table) are very different to the index. We have a very large active positions.

We hold specific industry leaders such as Anheisser Busch Inbev – a leader in the beverage market.

We hold Colgate – makers of toothpaste around the world. We hold Total – Europe’s leader in oil and gas production.

We don’t hold these companies because they’re included in the Index or have driven returns. We hold them for very different reasons.

Consider the recent Amazon Wholefoods acquisition as an example.

The consumer staples sector shows how we like to research, stay patient and use disruption to our advantage.

We focus on the best businesses, understand fundamentally how they work, then stay patient and wait until they are out of favour.

There is no doubt the Amazon Wholefoods deal will change food distribution globally.

As a result of this disruption the market discounted the sector as they questioned the brand value longer term post the deal.

We looked at the industry differently and focused on market share and their return on investment (ROI).

It was clear you only wanted to focus on P&G and Colgate with greater than 60% market share and 100% ROI.

We never wanted to own Kraft Heinz, Campbell soup or Kellogg’s due to their lower market shares — even though they were larger in the index.

Think differently to drive different results

Overall I believe you need to think differently, have a concentrated highly active and very selective stock picking approach,

Think like an owner in a group of #1 unique premium assets, be patient on valuation and get paid a dividend to wait while the business normalises.

This will serve you well as we enter the next decade.

This article has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and the information contained within is current as at August 22, 2019. It is not to be published, or otherwise made available to any person other than the party to whom it is provided.

PFSL is the responsible entity and issuer of units in the Pendal Concentrated Global Share Fund (Fund) ARSN: 613 608 085. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1800 813 886 or visiting www.pendalgroup.com. You should obtain and consider the PDS before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This article is for general information purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information in this article may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information in this article is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance.

Any projections contained in this article are predictive and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.